Beef, Poultry & Pork Market Update

7/1/26

Highlights

Beef

The beef complex was generally steady to firm this week despite ongoing tight fed cattle supplies and lighter harvest levels. Rib and loin items were mostly steady to slightly higher, reflecting continued foodservice demand heading into the holiday period. Chuck items were mixed, with clod products softer while chuck rolls held steady. Round cuts remained mostly steady to slightly higher, while briskets continued to improve. Ground beef markets strengthened as lean trim availability remained supportive of grinding demand.

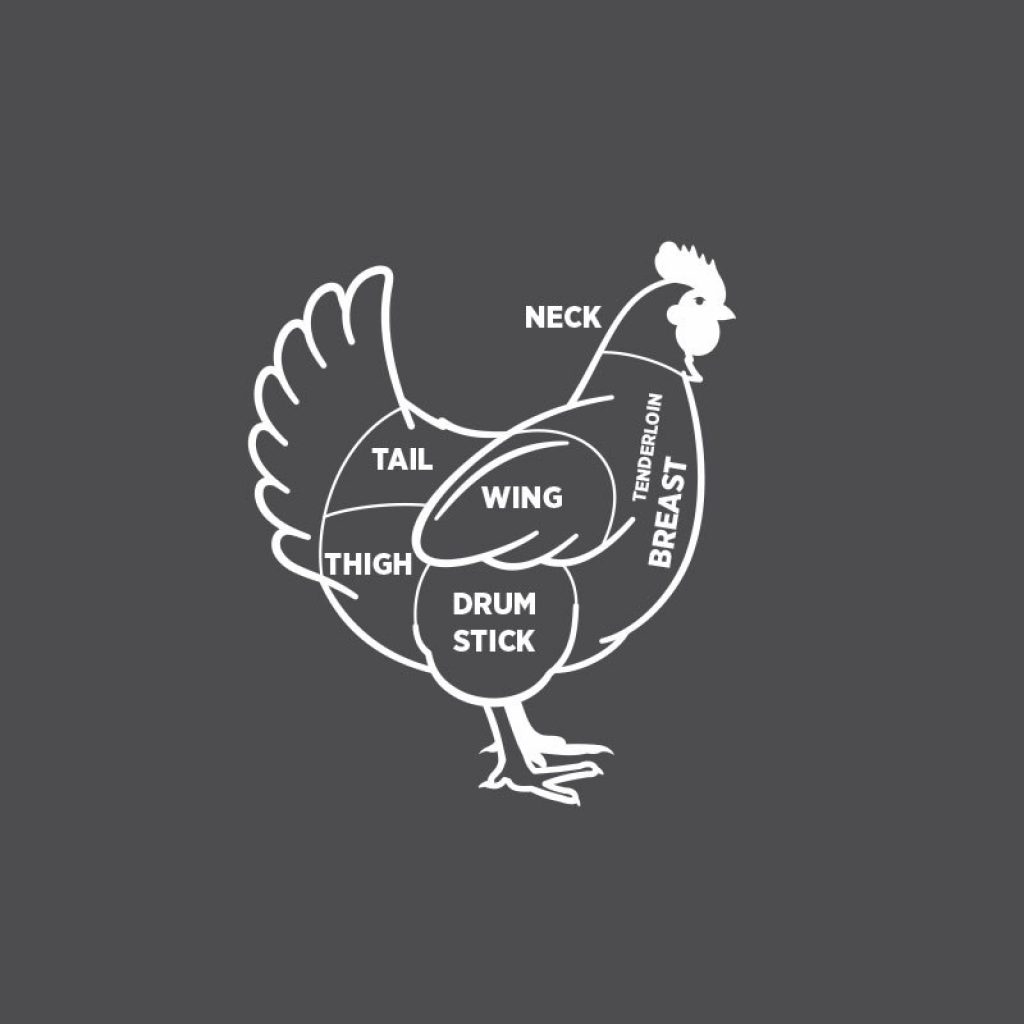

Poultry

Chicken markets remain split as the industry continues to see a feast-or-famine environment heading into the Fourth of July holiday. Wings remain the strongest segment of the complex with tight spot availability supporting values, while tenders and thigh meat continue to face pressure from ample supplies. Breast meat and whole birds are holding steady, and leg quarters, drumsticks, and bone-in thighs remain balanced as holiday demand approaches.

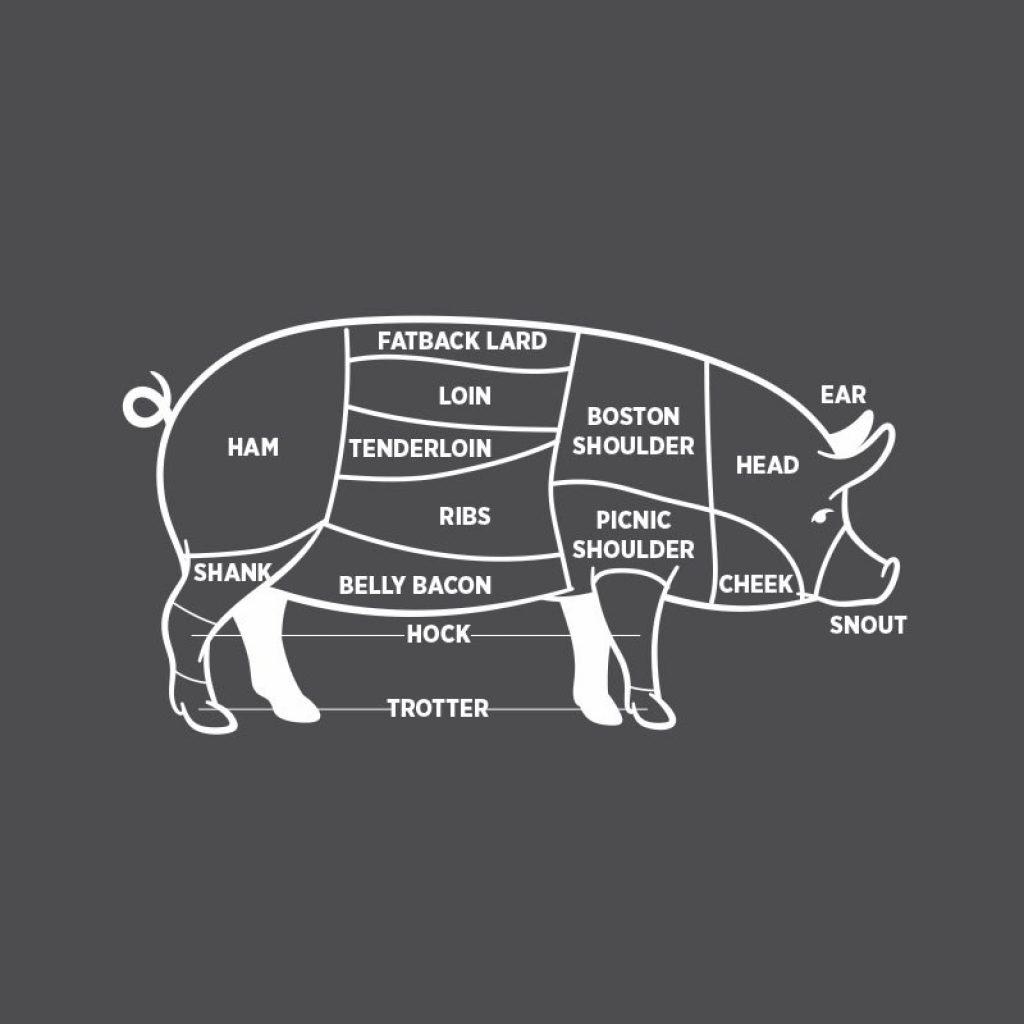

Pork

Pork markets softened this week as the belly complex experienced a sharp correction following several weeks of gains. The overall pork cutout drifted lower, while hog supplies remain adequate and slaughter levels continue at seasonal rates. Demand remains steady, but softer export activity and pressure on packer margins created a more cautious tone across the complex. Most primal values remain balanced, with bellies seeing the most volatility.

Bacon

Belly markets moved sharply lower this week following an abrupt midweek selloff that erased much of the recent rally. Bacon pricing reflected the softer belly market, ending a multi-week run of increases. Near-term market expectations call for steady to lower belly values over the next one to two weeks before seasonal demand begins providing support later in July. Supplies remain manageable, but demand signals have become more cautious in the short term.

Chicken

Whole Birds (WOGs) – Steady

Boneless / Skinless Breasts – Steady

Tenders – Down

Whole Wings – Up

Drumsticks – Steady

Leg Quarters – Steady

Bone In Thighs – Steady

Boneless / Skinless Thighs – Down

Pork

Bellies – Down

Spareribs – Steady

Hams – Down

Loins – Steady

Back Ribs – Steady

Tenderloins – Steady

Butts – Down

Picnic – Steady

Cushion – Steady

Fat Trim – Steady

Lean Trim – Up

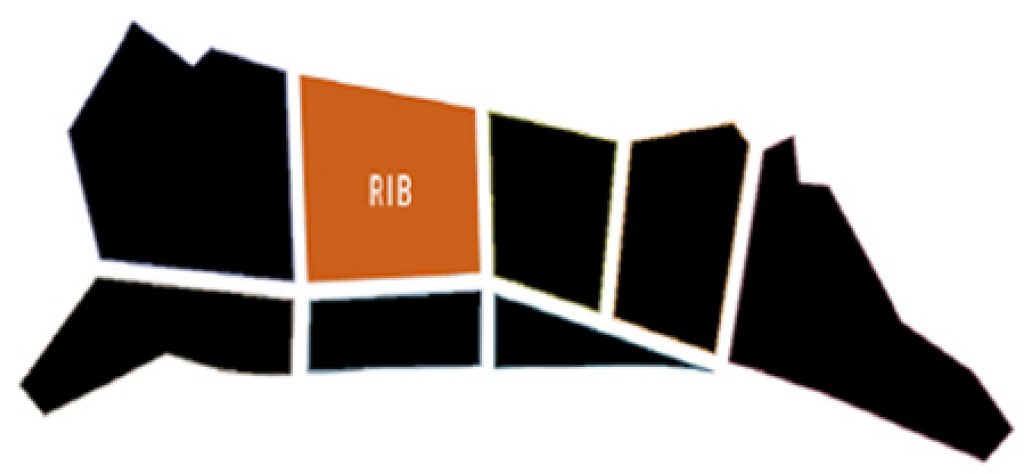

Beef subprimals USDA Choice for delivery week of 7/6/26.

Ribs

Ribeye Light – Up

Ribeye Heavy – Up

Loins

Strip Loin – Steady

Top Sirloin – Steady

Tenderloins – Steady

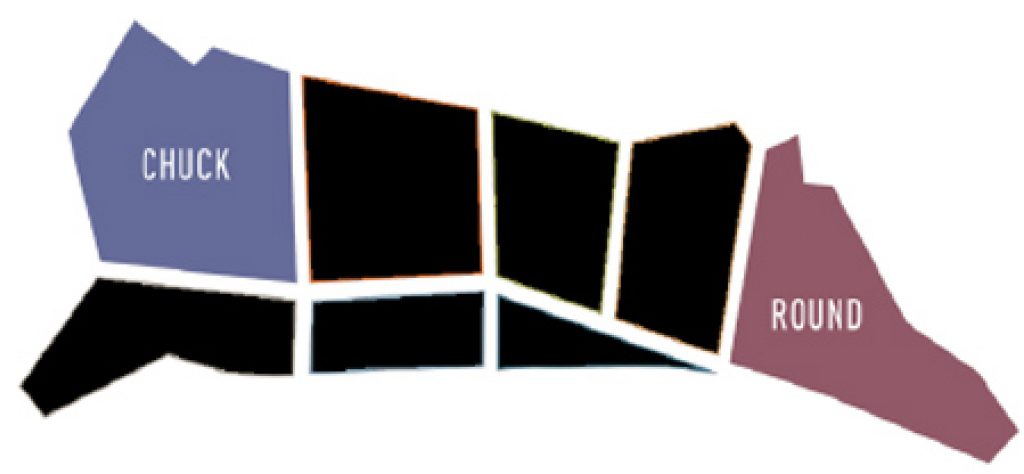

Chucks & Rounds

Chuck

Roll – Steady

Clod Heart – Down

Clod Tender – Steady

Chuck Flap – Down

Top Inside Round – Up

Outside Round – Steady

Thin Meats

Briskets – Up

Top Inside Round – Up

Outside Round – Steady

Flank Steak – Down

Outside Skirt – Up

Ground Beef

Ground Beef 73% – Up

Ground Beef 81% – Up

Ground Chuck – Up